Is Good To Put Money In A Roth Ira At Age 55

12 Min Read | Jan 18, 2022

At that place are some points in your life where you have to pick a side: Friends or Seinfeld? Curiosity or DC Comics? Michael Jordan or LeBron James?

Equally of import as those questions are for you lot and your friends, there's 1 contend that could really take a huge affect on your future—your retirement future: Roth IRA or 401(k) . . . which one is meliorate?

No matter what your retirement dream looks similar, you'll need money to turn those dreams into a reality. Afterward all, those summer vacations you want to take or that lake house you lot've ever wanted aren't going to pay for themselves! And the truth is that a Roth IRA and a 401(k) are both not bad means to build wealth for retirement.

Once you understand how both plans piece of work, you tin can meet how they tin can piece of work together to help y'all maximize your savings. And that's not only fancy investing talk. Your choices today could result in thousands—if non millions—of dollars downwards the road! Let'southward become ahead and dive right in, shall nosotros?

What Is a 401(k)?

A 401(g) is a retirement savings plan many employers offer as a way to encourage employees to save for retirement. Basically, you tell your employer how much you lot want to invest in your 401(k)—usually as a percentage of your salary or a specific amount each pay period—and that money is automatically taken out of your paycheck and put into retirement savings. Voila!

According to Ramsey Solutions' The National Study of Millionaires, 8 out of 10 everyday millionaires built their wealth through their visitor's 401(k). If all those millionaires could employ the boring, old 401(k) to get to millionaire status, then can you!

Advantages of a 401(g)

Allow'southward take a look at some of the main advantages of a 401(k):

- College contribution limits. In 2022, yous can investupward to $twenty,500 a yearin a 401(thousand), 403(b) or inmost 457(b) plans—not including the employer match. That'south a lot of coin! If you're l or older, you lot can add an additional $6,500 per year, for a full of $27,000.1

- Employer friction match. This is the large ane! Probably the best thing about a 401(k) plan is that your employer can match your investment up to a certain amount. That's a 100% return on your investment correct off the bat! Matching isn'trequired by the government, so not all employers offer it. If yours does, make the most of it. Don't overlookfree money!

- Your contributions lower your taxable income. Since y'all invest in your 401(yard) with pretax dollars, that means you'll pay less in income taxes when taxation flavor rolls effectually. Sad, non deplorable, Uncle Sam!

- Y'all can have information technology with you. And here's some peace of listen: The money you lot invest in your 401(m) isall yours. You tin can roll over your 401(one thousand) account to a Roth IRA if you get a new job or your company goes out of concern.

Disadvantages of a 401(k)

Your 401(k) is a great fashion to salve for retirement, only you also need to understand a few of its shortcomings too:

- Fewer options for mutual funds. Your employer ordinarily hires a 3rd-party administrator to run the company's retirement programme. That administrator picks and chooses which mutual funds you tin can invest in, limiting your options.Womp-womp.

- Your withdrawals in retirement will be taxed. Retrieve those tax breaks you get on your 401(k) contributions? Well, there's a catch. Since you fund a 401(chiliad) with pretax dollars, yous won't pay taxes at present, but y'all will pay taxes on that money in retirement. This could lead to a pretty hefty tax bill depending on what taxation subclass yous're in when you retire.

- Required minimum distributions (RMDs).Y'all can't leave your coin in your 401(k) forever. Get-go at age 72, youmust showtime withdrawing a certain amount of your savings each year, or yous'll pay a penalty.2 Also—there are penalties for withdrawing money before age 59 1/ii. Either manner, Uncle Sam wants his share!

- Waiting flow. If you're new to a company, you may have to wait a certain length of time to participate in a 401(k) programme or receive an employer match. That's not great, merely some things are worth the wait!

Now that we've broken downwards the 401(k), let'due south turn our attention to the one and but Roth IRA. So nosotros'll compare the two and encounter if in that location's a clear winner!

What Is a Roth IRA?

A Roth IRA (Private Retirement Account) is a retirement savings business relationship you can open yourself. When you lot hear the give-and-takeRoth, your ears should automatically perk up—because a Roth IRA allows your savings to grow tax-free . That's correct: tax-free. That means in one case you turn 59 i/2, you tin withdraw money from your account, and you won't owe a penny in taxes!

Advantages of a Roth IRA

Here are some advantages a Roth IRA has over a 401(1000):

- Taxation-complimentary growth. Unlike a 401(k), yous contribute to a Roth IRA withafter-tax money. Translation? Since you invest in your Roth IRA with money that's already been taxed, the money inside the business relationship grows tax-free and y'all won't pay a dime in taxes when you withdraw your money at retirement. And here's the bargain: In one case you're gear up to retire, the majority of the money in your Roth will exist growth. So, no taxes on that growth ways hundreds of thousands of dollars stay in your pocket. That's worth a happy dance!

- More investing options. With a Roth IRA, you're not express past some tertiary-party administrator deciding which funds you can invest in—you literally have thousands of mutual funds to pick and cull from. When you accept more options, you have more power to make good choices!

- Not tied to your employer. Unlike a workplace retirement plan, you can open a Roth IRA at whatsoever time. And no affair what your employment situation is, it doesn't bear upon your Roth IRA at all. No demand to roll over anything or worry about keeping track of a pile of 401(yard)s y'all left backside from one-time jobs!

- No required minimum distributions (RMDs).With a Roth IRA, y'all can proceed your coin in the business relationship forever if you'd like. That means you can let more of your money go on growing over a longer period of time!

- The spousal IRA. If you lot're married but just i of you earns money, you can yet open a Roth IRA for the nonworking spouse. The spouse who earns coin can invest in accounts for both spouses—upwardly to the full corporeality! On the other hand, only the employee of the visitor offer a 401(k) tin can contribute to their 401(k).

Disadvantages of a Roth IRA

The Roth IRA sounds pretty crawly, doesn't it? Unfortunately, the Roth IRA does have some limitations that you demand to exist aware of:

- Lower contribution limits. You tin can only invest up to $6,000 in a Roth IRA each year or $7,000 if you're age 50 or older.iii When you lot compare that with the contribution limits for a 401(k), yous might be thinking, That'south it? That'due south why 401(yard)due south and Roth IRAs work better together.

- Income limits. As amazing as the Roth IRA is, there's a hazard you might not even be eligible to put money into i. Gasp! If your modified adjusted gross income (MAGI) is higher than $144,000 equally a single person or more than $214,000 as a married couple filing jointly, then you lot won't be able to contribute to a Roth IRA in 2022.4 But don't worry, the traditional IRA is still an choice—information technology's better than nothing!

- The 5-year rule. This won't be an issue for nearly folks, simply the 5-year rule says you tin can't accept money out of your Roth IRA until information technology's been at least five years since you first contributed to the business relationship. You'll get hit with taxes and penalties if you break that rule (so don't do that). And recall: Just like the 401(yard), you'll be penalized for taking money out of a Roth IRA earlier age 59 1/two (don't do that, either).

Roth IRA vs. 401(k): What Are the Major Differences?

Okay, folks, does anybody else experience like they've been drinking water from a firehose? That was a lot of information! Here's the tale of the tape showing how the Roth IRA and the 401(thousand) stack upwardly against each other:

| Characteristic | 401(k) | Roth IRA |

| Eligibility | Only available through employer-sponsored programs. May be a waiting period before enrollment. | Must accept earned income, only restrictions utilise after a certain income based on your filing status. Married couples with only one income earner may open a spousal Roth IRA. |

| Taxes | Contributions are made with pretax dollars, lowering your taxable income. Y'all'll pay taxes on any money y'all withdraw in retirement. | Contributions are made with after-revenue enhancement dollars, assuasive investments to grow tax-gratuitous. No taxes on withdrawals in retirement. |

| Contribution Limits | For 2022, $xx,500 per year ($27,000 per yr for those 50 or older). Additional contribution limits may utilise to Highly Compensated Employees (HCEs). | For 2022 and 2022, $6,000 per twelvemonth ($7,000 per year for those age 50 or older). |

| Employer Contribution | Many employers offer a match based on a pct of your gross income. | No matching contribution. |

| Required Minimum Distributions (RMDs) | First at historic period 72, you lot must start taking out a certain amount each year (RMD) to avoid penalties. | No RMDs. The money tin can sit down in your account equally long as you alive. |

| Investment Menu | Account is controlled past a 3rd-party administrator who handles (and limits) investment options. | A wider variety of investment options and more control over how you lot invest. |

| Penalties | Penalties for withdrawals before 59 ane/2. | Penalties for withdrawals before 59 1/2. |

How to Brand a 401(k) and Roth IRA Piece of work Together

OK, so now we've arrived at the moment of truth: Should you put your coin in a 401(k) or a Roth IRA? The answer is . . . yep!

We filter out sleazy advisors. See upward to five investing pros nosotros trust.

If you're eligible for a 401(chiliad) and a Roth IRA, the all-time-case scenario is that you invest inboth accounts (and if yous tin can max them both out—knock yourself out!). That way, you lot're taking advantage of your employer matchand getting the tax benefits of a Roth IRA.

The all-time way to remember where to start is with this dominion: Lucifer beats Roth beats Traditional. An employer match is gratis money, and yous simply don't leave free coin on the tabular array—and so that's where you lot start!

After that, you take the taxation advantages of Roth accounts like a Roth IRA (tax-gratuitous growth and withdrawals in retirement) over traditional IRAs and their tax-deferred growth (which means taxes on withdrawals in retirement) every time. It pays off more in the long run!

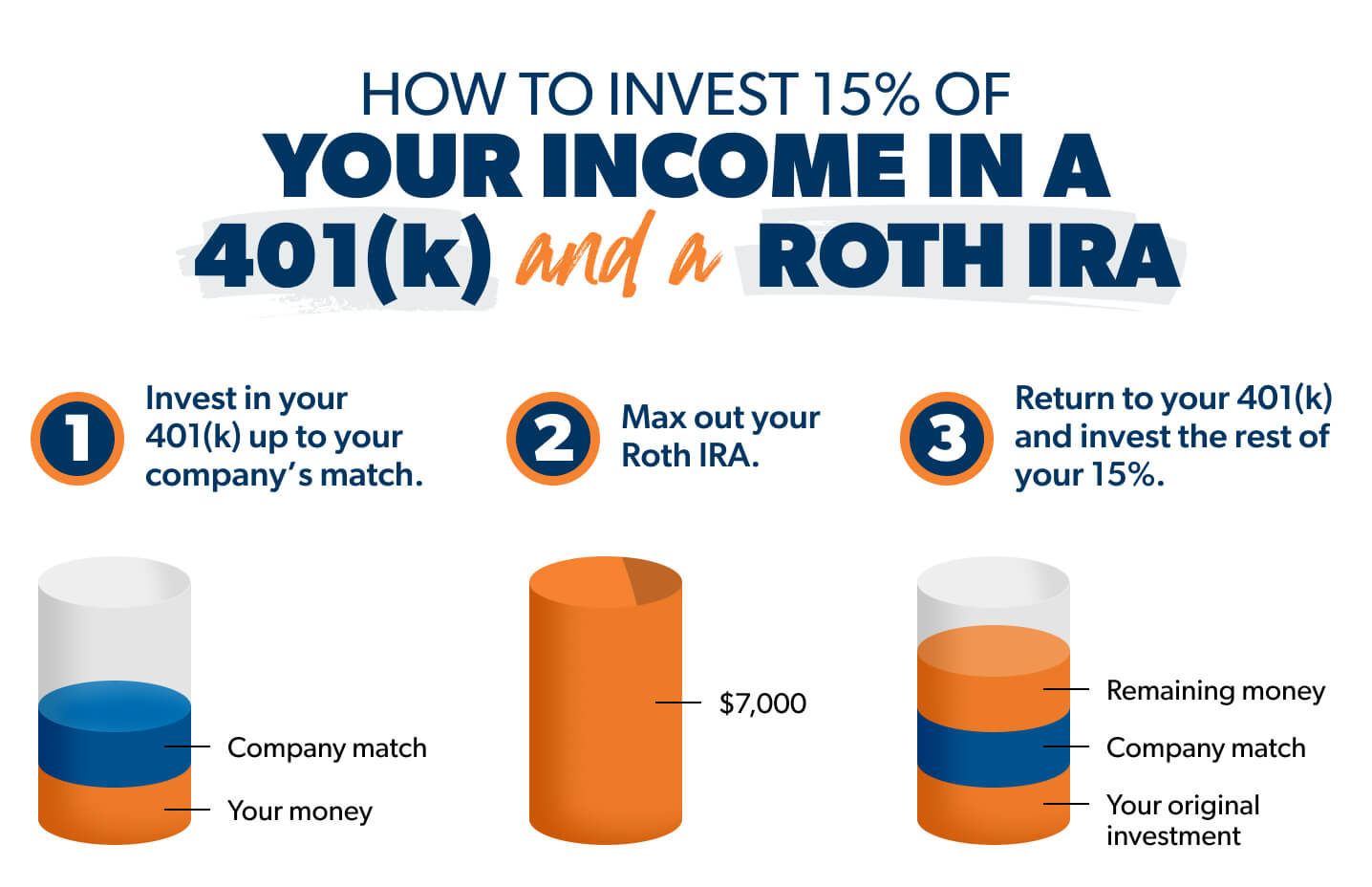

Here'due south how that works in iii simple steps: Let'due south say you lot make $60,000 a year and yous're under fifty. In one case you're debt-costless and have a fully funded emergency fund, your goal is to invest 15%—$9,000 in this case—in retirement.

- Yous start by investing in your 401(thousand) upwardly to the match your company offers. Let's say, in this example, that information technology's 3% of your gross income ($1,800). You lot invest $1,800 in your 401(thousand) to reach the employer lucifer. This leaves you with $7,200 more to invest.

- And then, you max out your Roth IRA. You tin only contribute $half dozen,000 in 2022, so that leaves y'all with $1,200.

- Return to your 401(k)and invest the remaining $ane,200.

Retrieve, if yous're older than l and behind on your retirement savings, you tin brand catch-upwards contributions to max out your Roth IRA at $7,000 and your 401(m) at $27,000 in 2022. Oh—and recollect this about the employer match on your 401(k): While it's nice to have, don't count it toward your 15% goal. Recall of it similar icing on the block of your own contributions.

Some companies offer a Roth 401(k), which combines many of the benefits of a 401(k) and a Roth IRA. If you work at a company with a Roth 401(thousand), that makes your situation a lot easier. If y'all like your investment choices inside the plan, you can but invest your entire xv% in your Roth 401(g) and y'all're done!

The Best Choice

Then, to sum it all upwards: Your best choice is to invest in your 401(k) upwards to your match and then invest in a Roth IRA—and make sure you reach your goal to invest 15% of your gross income in retirement!

E'er seek good advice and invest in skillful growth stock mutual funds with a history of potent returns. They're the best way to employ the power of the stock market place to build wealth over the long term. And steer articulate of trendy, "sophisticated" stuff like the latest "hot" unmarried stock, precious metals or cryptocurrency. Keep things simple and never invest in anything you don't empathise!

Here's the deal: Investing is worth the difficult work. If you don't relieve and invest now, you lot won't have annihilation to alive on in retirement. It's a big goal, simply you don't have to do this lonely.

Talk with aninvestment professional similar ane of our SmartVestor Pros. Get someone on your squad who will aid you stay focused and chasing your dreams. They can walk you through your investment options and create a plan for your situation.

Discover a SmartVestor Pro in your surface area!

Nigh the writer

Ramsey Solutions

Thank you! Your guide is on its fashion.

Invest With a Pro Who Gets This Stuff

Your future is too important for guesswork. Become help from a SmartVestor Pro today.

Find Your Pro

Invest With a Pro Who Gets This Stuff

Your future is too important for guesswork. Become assistance from a SmartVestor Pro today.

Find Your Pro

Source: https://www.ramseysolutions.com/retirement/401k-vs-roth-ira

Posted by: hensonpromes98.blogspot.com

0 Response to "Is Good To Put Money In A Roth Ira At Age 55"

Post a Comment